Information from the accounting and budget of the Ministry of Labour and Social Affairs for 2024 is considered reliable after corrections

PRESS RELEASE ON AUDIT NO 24/19 – 11 August 2025

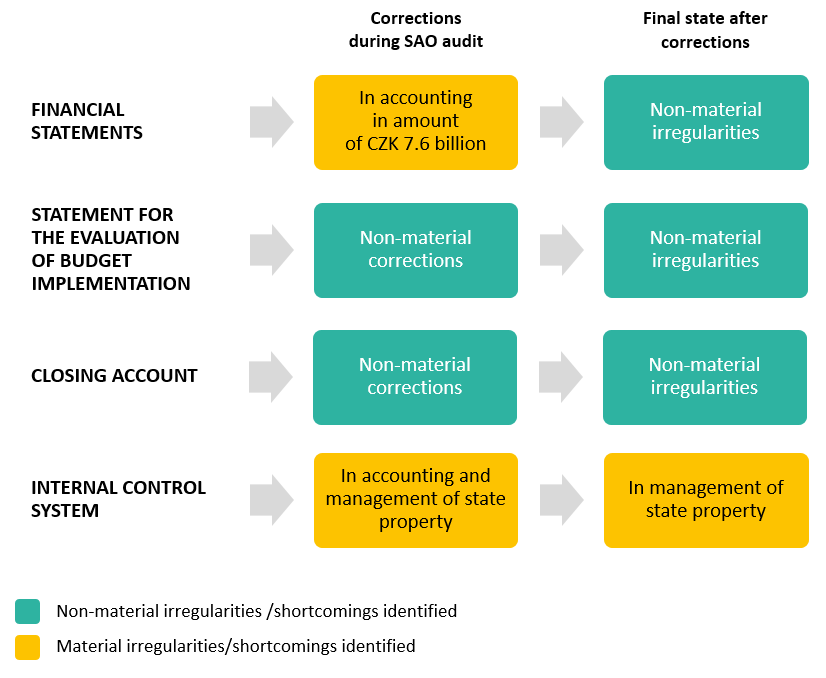

The Supreme Audit Office (SAO) has reviewed the closing account, accounting, the financial statements and the data submitted by the Ministry of Labour and Social Affairs (MoLSA) for the evaluation of the state budget implementation for 2024. As the audit began during the 2024 accounting period, the MoLSA was able to continuously correct the deficiencies identified by the auditors. The reviewed data is therefore considered reliable following the corrections made.

In its examination of the ministry’s accounting records, the SAO identified errors amounting to CZK 7.6 billion, which would have had a significant impact on the balances of items in the MoLSA’s 2024 financial statements. These related mainly to incorrect accounting of receivables and to items recorded in off-balance-sheet accounts. The MoLSA corrected the identified accounting errors and also implemented appropriate systemic measures. After these corrections, the SAO concluded that the MoLSA’s accounts were kept in compliance with the law and that the financial statements give a true and fair view of the subject matter of the accounting.

The closing account of the MoLSA and the data it submitted for the evaluation of the state budget implementation for 2024 did not contain material irregularities. These figures are therefore, according to the SAO, reliable.

The SAO also reviewed all measures taken to remedy the shortcomings identified in its previous audit from 2018 (Audit No 18/26). In 2020, the MoLSA informed the government that all necessary measures from that audit had been implemented. However, the auditors found that the MoLSA had not implemented five of the sixteen measures effectively and correctly by 2024. Consequently, the MoLSA did not provide the government with reliable information in 2020. Had the MoLSA effectively implemented all measures, it would not have been necessary in 2024 to make corrections amounting to CZK 5.9 billion (total errors would then have been CZK 1.7 billion instead of CZK 7.6 billion).

The internal control system of the MoLSA, following the measures adopted during Audit No 24/19, was assessed by the SAO as effective, with the exception of the area of management of state assets. This exception was due to the long-term failure to carry out regular inspections on the licences for purchased software. The SAO had already noted this breach of the MoLSA’s obligation to carry out such government-required inspections in the previous audit.

Communication Department

Supreme Audit Office