Ministry of Finance failed to evaluate the impact of the receipt lottery on tax collection, unnecessarily paid CZK 14 mill. and made mistakes in investment projects and land leases

Press release on Audit No. 21/12 – 4 July 2022

The SAO examined the management of the Ministry of Finance (MoF) between 2019 and 2020. The audit focused mainly on two financing programmes1, land leases and expenditure related to the receipt lottery. The SAO identified a number of shortcomings. For the receipt lottery, the MoF did not evaluate how it helped with the collection of taxes, which was supposed to be its purpose. In addition, the MoF concluded a contract with the supplier, on the basis of which it had to pay the full price even at a time when the lottery was no longer in use and the system was only maintained, which cost almost CZK 14 million. The audit also showed that the MoF failed to properly prepare investment projects. When choosing them, the MoF did not consider the current needs of the financial sector and fundamentally changed their form and costs at a time when the investment projects were already running. Other shortcomings also related to land leases.

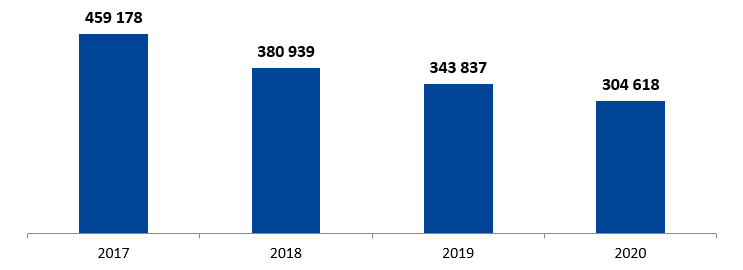

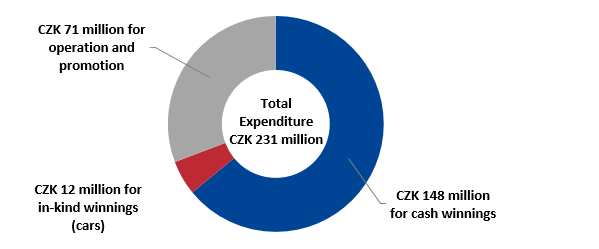

The receipt lottery was intended to motivate citizens to take receipts from merchants and thus encourage proper collection of taxes. After the end of the lottery, the MoF did not evaluate its contribution, although it paid a total of CZK 231 million for it. The largest part, almost CZK 160 million, consisted of cash or in-kind winnings for lottery participants. There were an average of 372,000 active lottery players per month, with the number decreasing each year.

The MoF concluded a contract for the operation of the lottery with the contractor for an indefinite period. In the end, the lottery lasted nearly four years even with a one-year notice period. As the contract did not specify the procedure for the early termination of the lottery, the MoF paid the full monthly rate to the contractor even at a time when the lottery was no longer in use and the system was only maintained, for which the MoF paid the supplier almost CZK 14 million.

Average monthly number of active players in the receipt lottery

Source: SAO audit report No. 21/12

Receipt lottery expenditure 2017-2021

Source: SAO audit report No. 21/12

Shortcomings in the planning of investment projects can be documented, for example, in the reconstruction of the MoF’s kitchen. In its preparation, the MoF stated that existing technologies are inadequate, equipment is obsolete with frequent breakdowns and higher consumption of gas, water and electricity. Even during the reconstruction, the MoF increased the original amount of CZK 5.4 million to CZK 7.9 million, but in the end, it only spent less than three million. The result was the purchase of a tunnel belt washer and electric dumpling slicer, stating that the other devices were fully functional. The investment was terminated prematurely after two years.

In the case of the 2015 plan for the acquisition of X-ray baggage control equipment, a metal detection frame and hand-held metal detectors, the MoF estimated the investment of approximately CZK 5.1 million. In 2019, the MoF fundamentally changed the parameters of the investment and came to the assumption to spend almost CZK 34 million on it. Finally — after almost six years — the expenses associated with this investment amounted to CZK 2.1 million.

The auditors also focused on land leases. The SAO found that the MoF had been renting out extensive land at the exhibition grounds in Letňany in Prague with an area of almost 30 thousand m2 at an unchanged rental price. The MoF changed this rental price to the same tenant only when a new contract was signed in 2021, but with a fixed indexation of 2.6 % and without using the inflation clause. According to the Czech Statistical Office, inflation in 2020 reached 3.2 %. In addition, the tenant himself indicated an inflation of 4.5 % in the bids to conclude the contract.

Another of the deficiencies found consisted of the fact that the MoF carried out the ex-ante control prior to the commitment only as an ex-post control — i.e., for example, after the conclusion of the contract, the dispatch of the order, and in one case even after the delivery of the work. In more than half of the 85 audited cases, the ex-ante control was not carried out on time.

1] Programme 112V01 — Development and renewal of the material and technical basis of the Ministry of Finance management system since 2007 and programme 012V01 — Development and renewal of the material and technical foundations of the Ministry of Finance’s management system (for the years 2014-2020).

Communication Department

Supreme Audit Office